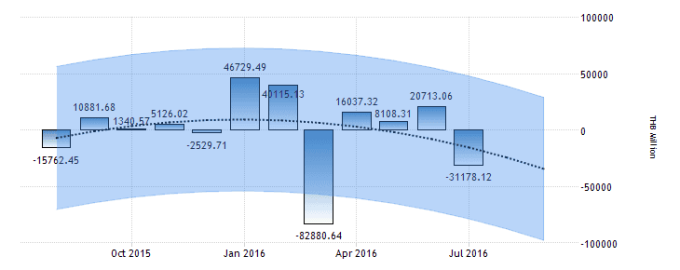

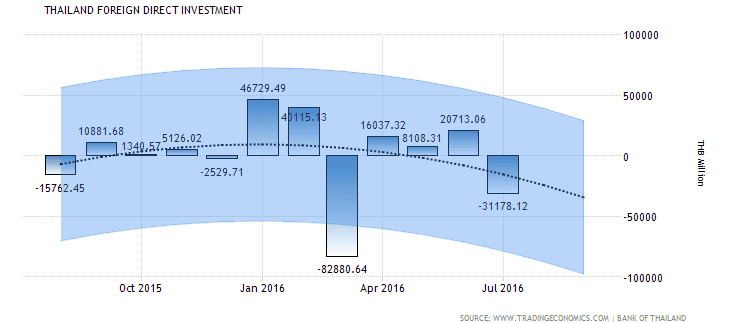

The Board of Investment of Thailand (BOI) has expanded its 2016 investment value target to 550,000 million baht ($ 16 Bln), an increase of about 20% from the previous target of 450,000 million baht

Improved political and economic situation enhance investment climate and investors’ confidence and New opportunities explored in overseas markets while actual investment activities in Thailand to be accelerated.

BOI manpower to be expanded to support more aggressive investment promotion Driven by political and economic recovery, the Board of Investment of Thailand (BOI) has expanded its 2016 investment value target to 550,000 million baht ($ 16 Bln), an increase of about 20% from the previous target of 450,000 million baht.

The new target was announced at the annual meeting, chaired by Deputy Prime Minister Somkid Jatusripitak, with the heads of the BOI’s 14 overseas offices today. Mr Somkid updated the meeting in Bangkok about the positive signal in political and economic recovery and global investment trend that moves toward Asia.

Considering such trend, he recommended BOI to increase manpower to support the expected increase in investment inflow and to grow new and existing markets across Asia, including Japan, Korea, China, India as well as Singapore.

“Other advantages, such as the benefits of using Thailand as the hub to grow business in China, ASEAN and India can be highlighted to draw more investment”

BOI has adjusted its application target from 450,000 million baht to 550,000 million baht. The 10 target industries will remain in focus. We hope to increase the proportion of investment in these target industries to more than 50% of the total investment application.

“Considering the very positive trend in investment applications, coupled with strong investors’ confidence towards economic and political development in Thailand, we are certain to achieve the new investment goal by the end of 2016.”

In the first seven months of 2016, the number of investment incentive applications by project increased by 77% while application value soared by 218%.

The BOI received 853 applications worth 320,720 million baht, up from 483 projects with a value of 100,740 million baht in the same period of 2015.

The value of project applications in the 10 target industries accounted for 43% of the total applications or 138,871 million baht, reflecting the success of investment promotion policy and execution. An investor confidence survey done by the BOI in May 2016 also showed a positive trend.

The survey, released last week, indicated that 32.8% of companies currently investing in the country have plans to expand their investment. The majority of respondents cited good infrastructure, sufficient supplies of parts and suppliers, efficient logistics and strong investment promotion incentives as key factors behind their decisions.

Meanwhile, investors’ concerns over political and economic instability have significantly decreased from the same period last year, showing overall improved confidence in Thailand’s political and economic development.

Investors’ concern over the government sector’s transparency has significantly dropped from 30.15% in 2015 down to only 19.38%. In addition, the increase in GDP growth from 3.2% in the first quarter this year to 3.5% in the second quarter contributed to improved confidence among investors and the business sector in the Thai economy and its outlook.

“Thanks to these positive factors, the overall investment outlook is promising,” said Mrs Hirunya.

To maintain and enhance the positive investment momentum and confidence, the BOI will continue its plan to promote Thai investment opportunities in major markets through international road shows. In the remaining four months, a total of more than 40 road shows are planned in major markets, such as Japan, South Korea, China and northern Europe. The BOI will also work closely with its partners worldwide, including leading organisations in the trade, investment and banking sectors.

Honorary investment advisers will provide information about investment opportunities and government support in Thailand.

“With a concerted effort from the BOI’s 14 overseas offices worldwide, local offices and concerned government organisations, we hope to attract more investment from foreign investors, especially in the 10 target industries that are crucial to supporting the transformation of Thailand to a knowledge-based economy. Coupled with the positive development trend and political and economic stability, the country’s strength as the gateway to ASEAN and South Asia, as well as the upcoming laws that enhance investment climate, including the new BOI law, Eastern Economic Corridor (EEC) law and the competitiveness fund law, Thailand is positioned well as the desirable investment destination,” said Mrs Hirunya.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}